Up to date valuations of assets are becoming ever more important – and the quality of that valuation can be critical. The last time anyone wants to discover it is missing or out-of-date is when a claim comes in and there are coverage issues.

Valuations are key for policyholders to:

- Prove ownership

- Describe the item, with a photograph

- Give a current true replacement value for insurance purposes

Professional and up-to-date valuations are also key for brokers, AR’s and insurers because:

- They help an underwriter correctly assess and price the risk – reducing the risk of underinsurance

- They make policy negotiation conversations easier – e.g. clarity over what is owned, how much is actually worn vs. kept in a safe

- Jewellery setting checks reduce the risk of loss/damage, and therefore claims

- Should an item be lost/damaged, it is easier and quicker to assess the loss and handle the claim with a detailed description and accurate valuation (reducing claim management costs for all)

- Better claims management = happier policyholder = higher retention (where you want to keep the client!)

- Indicative of a “good insured” – they have invested in, and take care of, their property.

So what’s the problem with “valuations” in the industry at present?

There are many issues that can arise:

- No valuation at all.

This could be because the item was a gift or has been recently inherited, or because the receipt or valuation has been lost/mislaid.Surprisingly, on visits to clients’ homes by valuers, high-value assets that are not specified (and therefore not covered) are often identified – simply due to oversight by the client. This could be a painting, a Hermes handbag collection, or jewellery the client has forgotten about. Many policyholders do not realise that a piece of furniture, a tapestry, or some books or antique ceramics are actually very valuable (hence the popularity of “Antiques Roadshow”!)Brokers are sometimes unable to visit clients’ homes due to time-pressure – which means this is a real but unrecognised risk. A home visit by a valuer can mitigate this.

- An out-of-date valuation.

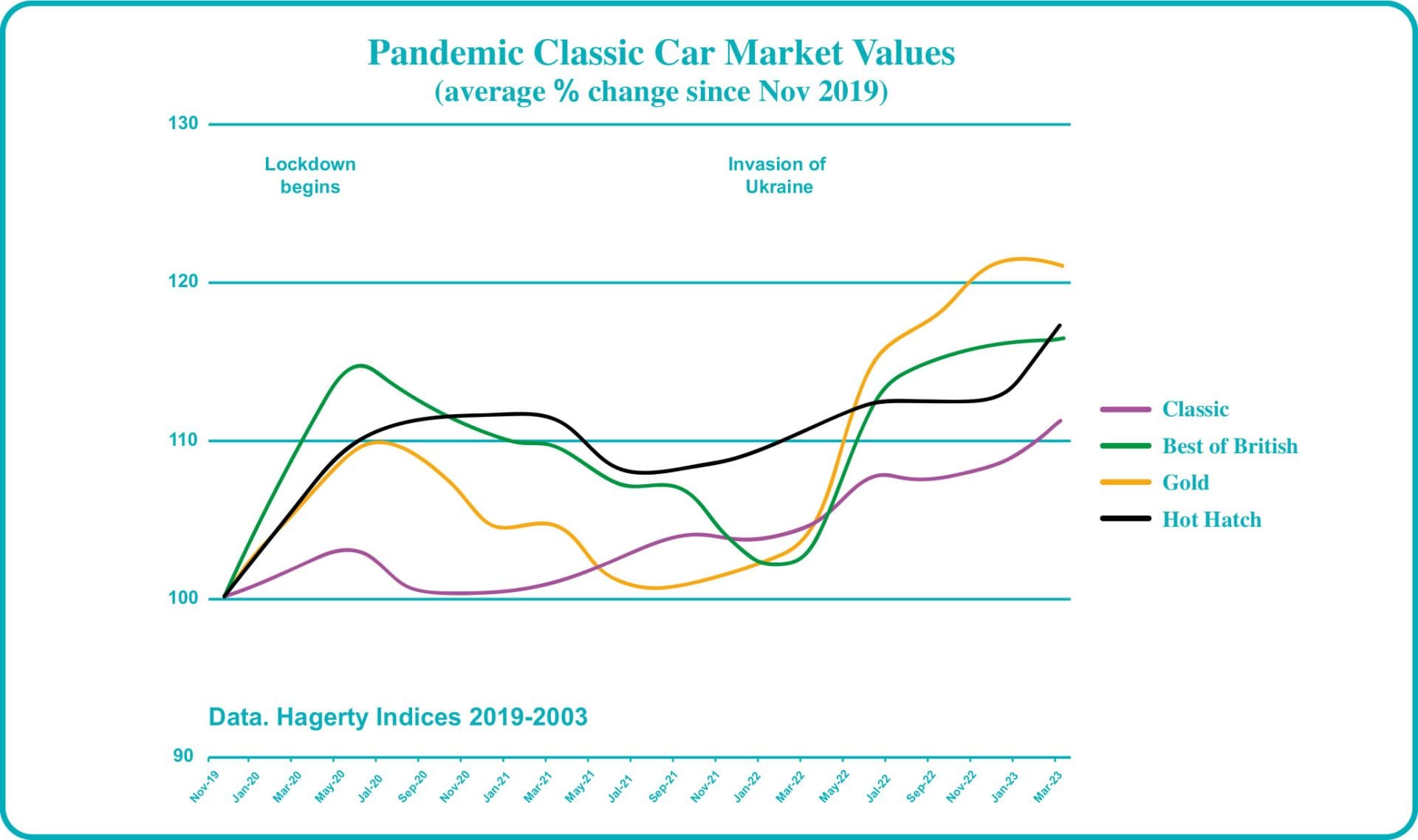

Prices for HNW assets can fluctuate dramatically, but at different levels over different time periods (see below). An out-of-date valuation will mean the item is underinsured, leading to underpayment at the point of claim.

- A simple purchase receipt.

This may state that £10k was paid for a diamond ring, but does not give enough information to replace it easily. It can also lead to underinsurance – as some collectible items can increase in value immediately after purchase.

- Unreliable valuations and receipts.

At the point of claim, an insurer may accept a receipt from Goldsmiths or Sotheby in the UK as evidence of an item having been purchased and owned. They are reputable companies, and the receipt will be in £’s sterling.What if there is an issue or error with a valuation? Does the company providing it carry PI in the UK? Do they have the expertise to correctly value an item? Do they follow industry best-practice standards e.g. FSQS? Are they GIA registered?A receipt or valuation may be from a company in Russia, or India, or Hong Kong. It may be written in that language, with no easy way of knowing whether the company is reliable and trustworthy. Is this a genuine purchase receipt, or could it be a fraudulent, inflated valuation? Even if genuine, it is still an issue for claims teams at the point of claim.What currency is the valuation in? Sterling, US dollars and Euros are currencies which can be reasonably relied upon. But how comfortable is a claims team with a valuation in Russian Rubles or Venezuelan Bolivars, currencies that can fluctuate wildly. What about a valuation in Bitcoin? What value should go in the policy – who decides?

Poor valuations typically lead to underinsurance, difficult claims handling for everyone (client, broker/AR and insurer), and even claims being rejected.

This underinsurance also means GWP can be left on the table for the insurer, and less commission is earned by the broker or AR.

What should a valuation contain?

A professional valuation will provide a comprehensive document that includes:

- An overall description of the item, including dimensions and overall condition

- For jewellery:

- details of the stone(s), including size and quality. If a stone is certified, the report number and date should be noted within the description, as well as the name of the grading laboratory.

- the metal and overall setting

- any marks (such as hallmarks or maker’s marks)

- a value, which should be dated and confirm the purpose/type of valuation

- confirmation that the clasps and settings of jewellery have been checked. This will help if a “clasps and settings” clause has been applied. It will also reduce the risk of loss or damage overall.

What’s happening in the HNW asset market at the moment?

Values change all the time. The replacement value for something bought 10 years ago will be different to the purchase price (if known). There is a common misconception that antiques have no value – it may be difficult to sell them, but can prove very costly to replace them if damaged or lost.

The costs of restoration and repair have increased exponentially. If an item of furniture or jewellery has been damaged, it can possibly be repaired – but this is likely to be at a substantial premium. It’s not just the time and skill of the artisan you are paying for, their rates, rents, stock and materials have all increased significantly.

Ceramics and glass from the early 20th Century are often overlooked by clients. These items are achieving record-breaking prices at auction – the owner may well not know this, but this can be spotted and a problem avoided during a home visit.

Paintings and artworks often represent some of the highest valued items in a home, yet little regard is paid to ensuring their insurance cover is up-to-date and adequate. The value of art can change/fluctuate significantly, and sometimes overnight (e.g. death of an artist). The value is often linked to taste and fashion – which artists are most desirable at the time. John Constable’s iconic “Hay Wain” was the Nation’s favourite artwork for generations; it has now been displaced by Banksy’s “Girl With Balloon”. How is a broker/AR to know during a client home visit whether the artwork on the wall is likely to be valuable and needs a proper valuation?

What’s the solution?

Clients should be encouraged to get a professional valuation of all their HNW assets done on a 3 yearly basis. If the client is a collector of watches, they should consider reviewing values annually – makers discontinue styles over time, thereby increasing their values.

For many clients, a home-visit is the quickest, easiest, and safest way to achieve this – as the valuer(s) will come to their home at a time of their choice. This helps ensure no potential HNW asset is left unidentified and unspecified.

Ideally, a valuer should be able to value all items (e.g. paintings, jewellery, watches, guns, clothing/shoes/handbag collections), not just some of them. A one-stop-shop service – with the right expert for each area.

A good valuation service will be FSQS registered – meaning they adhere to finance industry-recognised standards. This provides confidence in the quality of the valuation and the safety of customer data. They should also carry UK-based PI in case of a mistake or error.

Brokers and AR’s are critical in the valuation process. The client may need convincing to invest in a professional valuation – they are often not as expensive as many think.

A good valuation service will be happy to do an initial phone call with the broker/AR in attendance to explain the process, why this is so important, and the risks of not being correctly valued. Having the broker/AR at the site visit is also very useful, as it helps cement their relationship with their client, and helps them more fully understand the needs of their client.

Who are Doerr Dallas Valuations?

This article was written by Rachel Doerr of DDV.

Rachel has spent her career specialising in valuing HNW assets, setting up her own business to do so in 2016. The business is FSQS registered, and carries PI of £5m.

Doerr Dallas pride themselves on their relationships with brokers and ARs, and are keen to support them in many ways free-of-charge, for instance:

- Quotations, often including different cost options to meet the needs of different clients

- Training for staff

- Articles for websites and newsletters

- Presenters at events e.g. speakers, free valuations at a wine-tasting

- Joint phone calls to clients

- Reminders when the market has changed and certain items need revaluing

Doerr Dallas Valuations can help eliminate concerns about the correct valuations of a client’s HNW assets in all categories, for clients in the UK and across Europe. The team includes some of the most renowned and internationally recognised specialists in their areas of expertise – including Fine Art, Antiques, Silver, Jewellery, Watches, Classic Cars, Books and Manuscripts, and other valuable collectibles as well as handbags, wardrobe contents and general household contents.

Rachel can be reached on 01883 722736 or 07876653602 and email [email protected]